In Simple Terms: Interest rates are the cost of borrowing money, or the reward for saving it. They’re expressed as a percentage of the principal over a specific time period.

Types of Interest Rates

Simple Interest

Simple interest is calculated only on the original principal amount. It’s straightforward but less common in modern finance. Formula: I = P × r × t

Compound Interest

Compound interest is calculated on both the principal and previously earned interest. This creates exponential growth over time, making it powerful for long-term savings but costly for debt.

The Power of Compounding — $10,000 invested at 7% annual return:

- After 5 years: $14,026

- After 10 years: $19,672

- After 30 years: $76,123

Key Interest Rate Terms

- APR (Annual Percentage Rate): The annual cost of borrowing including fees. Used for loans and credit cards.

- APY (Annual Percentage Yield): The effective annual return including compounding. Used for savings accounts.

- Prime Rate: The rate banks charge their best customers. Many loans are priced relative to prime.

- Federal Funds Rate: The rate banks charge each other overnight. Set by the Federal Reserve.

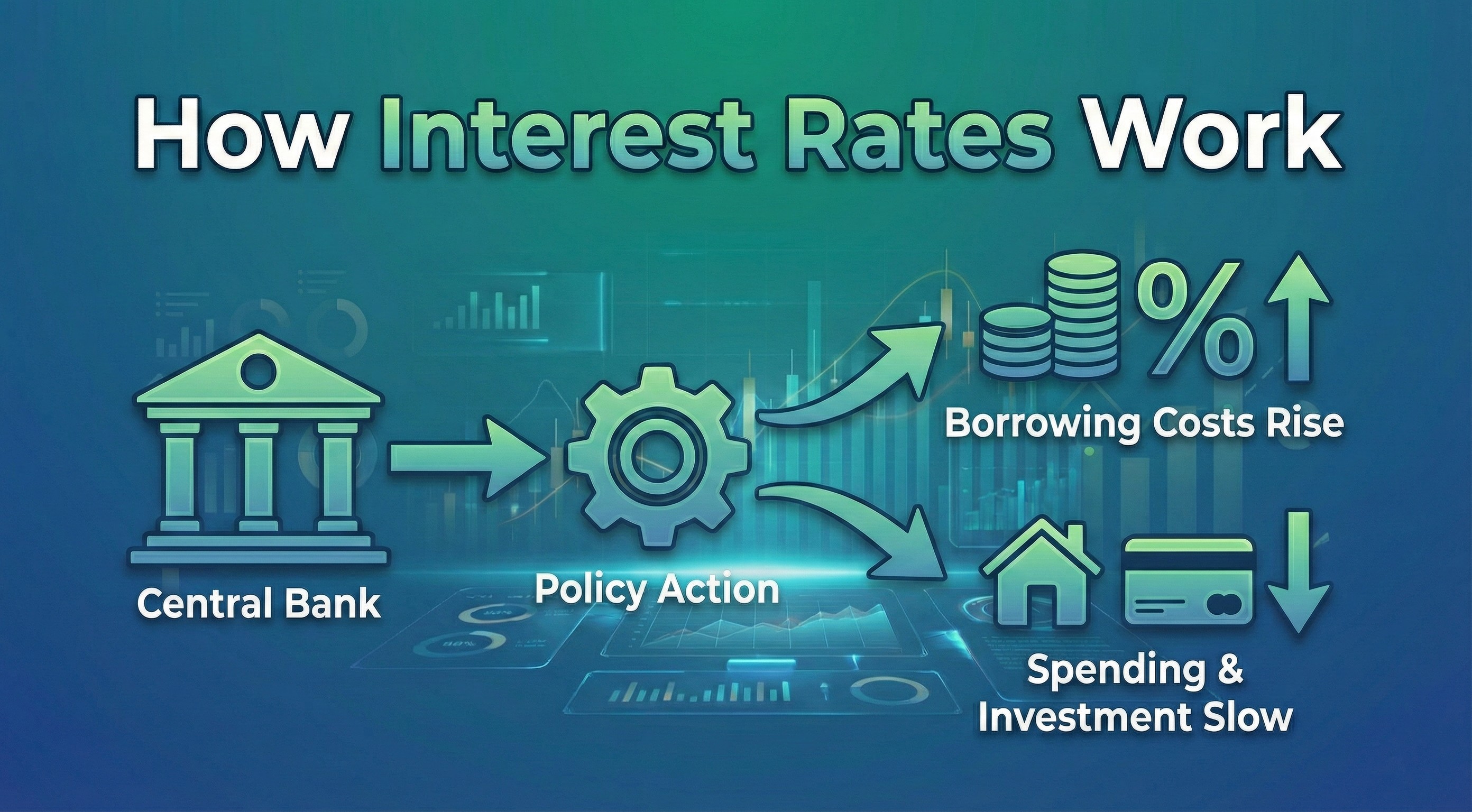

What Influences Interest Rates?

- Central Bank Policy: The Fed raises/lowers rates to control inflation and employment

- Inflation: Higher inflation typically leads to higher interest rates

- Economic Growth: Strong growth may push rates up; recessions push rates down

- Credit Risk: Higher risk borrowers pay higher rates

- Loan Term: Longer terms often (but not always) have higher rates

How Rates Affect You

When Rates Rise ↑

- ✓ Higher savings yields

- ✓ CDs and bonds pay more

- ✗ Mortgages cost more

- ✗ Credit card debt grows faster

When Rates Fall ↓

- ✓ Cheaper to borrow

- ✓ Refinancing opportunities

- ✗ Lower savings returns

- ✗ Retirees earn less on fixed income