Fixed vs Adjustable Rate Mortgage: Which Should You Choose?

When you apply for a home loan, one of the first — and most important — decisions you face is choosing between a fixed-rate mortgage and an adjustable-rate mortgage (ARM). Both options have real advantages, and the wrong choice could cost you thousands of dollars over the life of your loan.

This guide breaks down exactly how each works, compares them side by side, and helps you figure out which one makes sense for your situation.

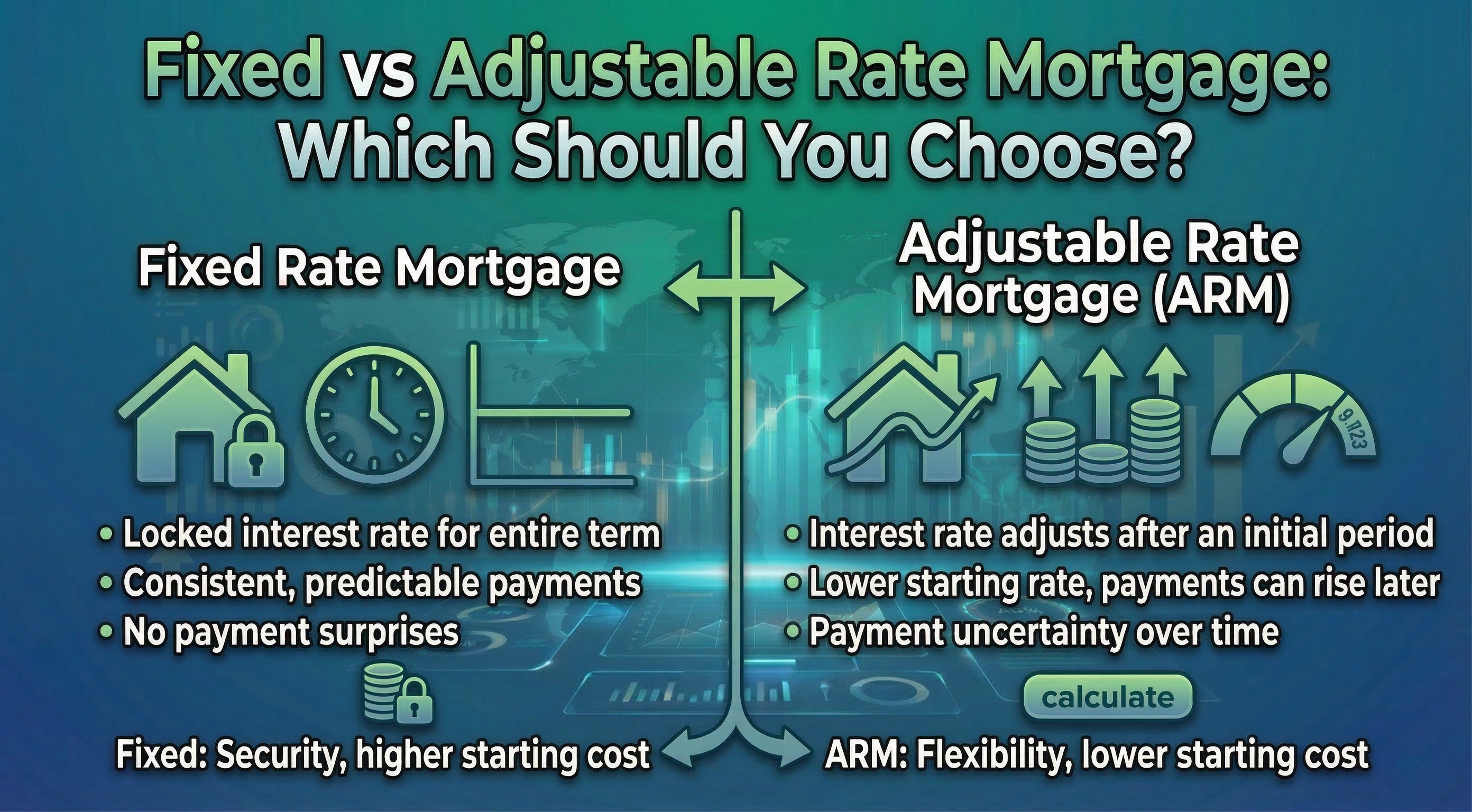

What Is a Fixed-Rate Mortgage?

A fixed-rate mortgage is a home loan where the interest rate stays the same for the entire life of the loan — whether that’s 10, 15, 20, or 30 years. Your monthly payment for principal and interest never changes, no matter what happens to market interest rates.

Key Features of a Fixed-Rate Mortgage

- Interest rate is locked in at the time of closing

- Monthly payment (principal + interest) stays the same throughout the loan

- Common terms: 15-year and 30-year, though 10- and 20-year options exist

- Easier to budget long-term since payments are predictable

- Higher starting rate compared to the initial rate of an ARM

Example: You take out a $300,000 30-year fixed-rate mortgage at 6.5%. Your principal and interest payment will be approximately $1,896 per month — every month for 30 years. If market rates rise to 8% two years later, your payment stays at $1,896.

Pros and Cons of Fixed-Rate Mortgages

| Pros | Cons |

|---|---|

| Predictable monthly payments | Higher starting interest rate than ARMs |

| Full protection from rising rates | No automatic benefit if rates fall (must refinance) |

| Easy to budget long-term | Refinancing costs money |

| Peace of mind and stability | May qualify for a smaller loan amount |

What Is an Adjustable-Rate Mortgage (ARM)?

An adjustable-rate mortgage starts with a fixed interest rate for an initial period — usually 3, 5, 7, or 10 years — and then adjusts periodically based on a market index. After the fixed period ends, your rate can go up or down, and your monthly payment changes with it.

ARMs are written in a format like “5/1” or “7/6.” The first number is how many years your rate is fixed. The second is how often (in years or months) it adjusts after that. So a 5/1 ARM has a fixed rate for 5 years, then adjusts once per year.

How ARM Rate Adjustments Work

When your ARM adjusts, the new rate is calculated by adding a lender margin to a financial index — typically the Secured Overnight Financing Rate (SOFR). Most ARMs also have rate caps to limit how much your rate can change:

- Initial cap: limits the rate increase at the first adjustment (commonly 2%)

- Periodic cap: limits how much the rate can change at each subsequent adjustment (commonly 1–2%)

- Lifetime cap: the maximum total increase over the life of the loan (commonly 5%)

Example: You take a 5/1 ARM at 5.5% on a $300,000 loan. Your payment for the first 5 years is ~$1,703/month. After year 5, if the index rises, your rate could adjust up to 7.5% (with a 2% initial cap), raising your payment to ~$2,052/month.

Common ARM Types

| ARM Type | Fixed Period | Adjustment Frequency | Best For |

|---|---|---|---|

| 3/1 ARM | 3 years | Every 1 year | Short-term owners (selling within 3 years) |

| 5/1 ARM | 5 years | Every 1 year | Those planning to move in 5 years |

| 5/6 ARM | 5 years | Every 6 months | Short-to-medium term buyers |

| 7/1 ARM | 7 years | Every 1 year | Medium-term homeowners |

| 10/1 ARM | 10 years | Every 1 year | Buyers wanting lower rates but longer stability |

Fixed vs Adjustable Rate Mortgage: Side-by-Side Comparison

| Feature | Fixed-Rate Mortgage | Adjustable-Rate Mortgage (ARM) |

|---|---|---|

| Interest Rate | Never changes | Fixed initially, then adjusts |

| Monthly Payment | Always the same | Can increase or decrease |

| Starting Rate | Higher | Lower (introductory rate) |

| Best Loan Term | 15 or 30 years | 3, 5, 7, or 10-year fixed period |

| Risk Level | Low — no surprises | Medium to High |

| Best If Rates Rise | Yes — you’re protected | No — your rate could go up |

| Best If Rates Fall | No — need to refinance | Yes — rate adjusts down too |

| Predictability | Very high | Low after fixed period |

| Best For | Long-term homeowners | Short-term owners or those expecting rate drops |

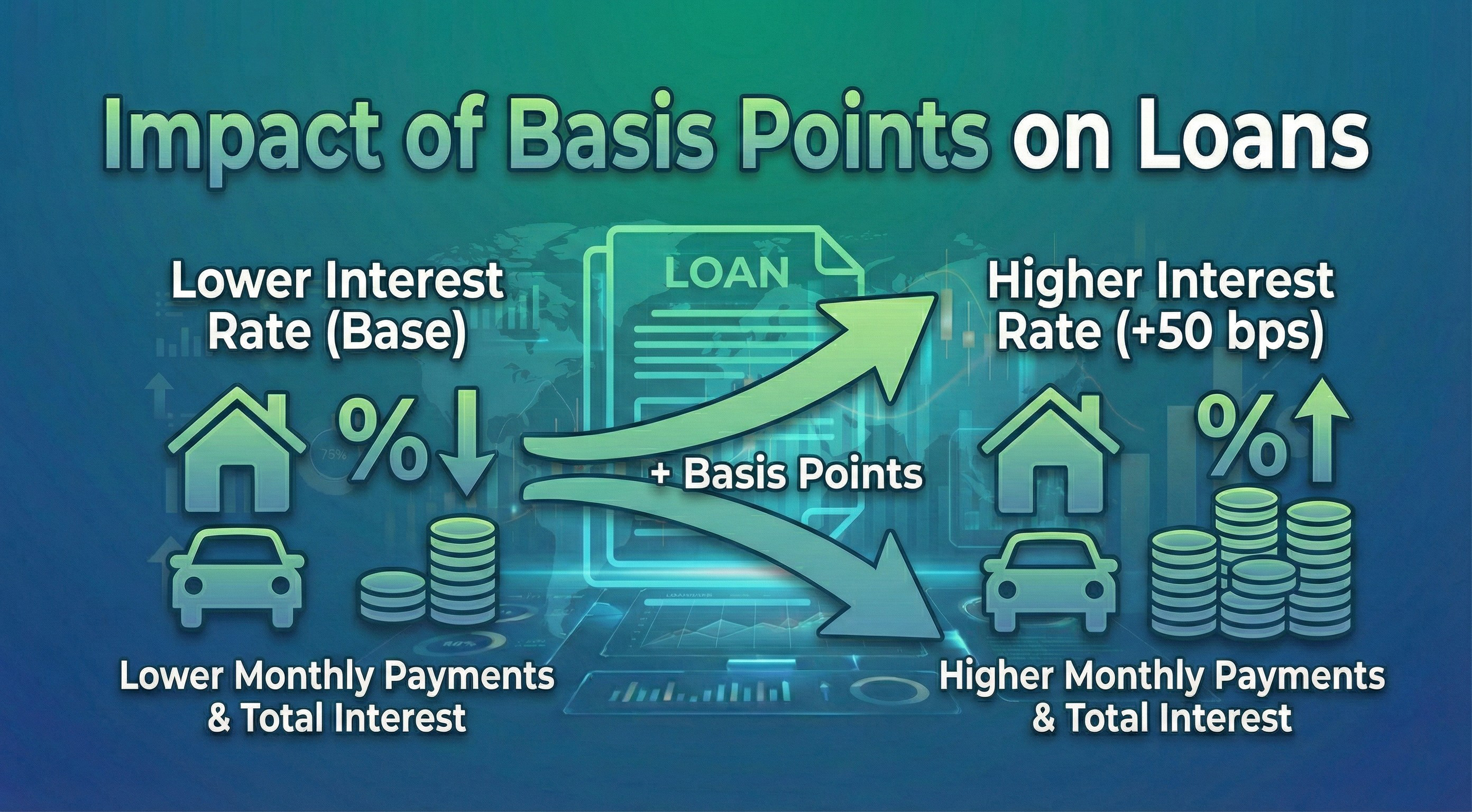

How Basis Points Affect Your Mortgage Rate

Mortgage rates are often discussed in basis points (bps). One basis point equals 0.01%, so 25 basis points = 0.25%. When the Federal Reserve raises or cuts rates, they typically do so in 25 or 50 basis point increments — and these changes directly affect both fixed and adjustable mortgage rates.

For a $300,000 mortgage, a 25 basis point difference in rate translates to roughly $45–$50 per month in payment difference. Over a 30-year loan, that small difference adds up to over $16,000 in total interest.

ARMs are especially sensitive to basis point changes because their rates are tied to a market index. A 100 basis point rise in the index (1.00%) directly increases your ARM payment once the fixed period ends.

Which One Should You Choose?

There is no single right answer — the best mortgage type depends on your personal situation.

Choose a Fixed-Rate Mortgage If:

- You plan to stay in the home for 7+ years

- You want predictable, stable monthly payments

- You are risk-averse or on a tight budget

- Current interest rates are historically low

- You have a consistent income without major fluctuations

Choose an Adjustable-Rate Mortgage (ARM) If:

- You plan to sell or refinance before the fixed period ends

- You expect interest rates to fall in the coming years

- You want a lower initial rate to qualify for a larger loan

- Your income is likely to increase significantly over time

- You’re buying a starter home with plans to upgrade in a few years

Quick Decision Guide

| Your Situation | Recommended Mortgage Type |

|---|---|

| Buying your forever home | Fixed-Rate |

| Staying less than 5 years | 5/1 ARM |

| Rates are currently high, expected to drop | ARM |

| Rates are currently low | Fixed-Rate |

| On a tight or fixed income | Fixed-Rate |

| Buying a second home or investment property | ARM (if short-term hold) |

| First-time buyer wanting simplicity | Fixed-Rate |

Frequently Asked Questions

Can I switch from an ARM to a fixed-rate mortgage?

Yes — you can refinance an ARM into a fixed-rate mortgage at any time. However, refinancing comes with closing costs (typically 2–5% of the loan amount), so it makes financial sense only if the new rate is meaningfully lower or if you plan to stay in the home long enough to recover those costs.

Is an ARM risky?

ARMs carry more risk than fixed-rate mortgages because your payment can increase significantly after the fixed period ends. However, rate caps limit how much your rate can rise. The risk is manageable if you plan to sell or refinance before the first adjustment.

What happens to my ARM if the Federal Reserve raises rates?

When the Fed raises rates, the market indexes that ARM rates are tied to (like SOFR) also tend to rise. This means your ARM rate will likely increase at its next adjustment. The actual increase depends on how much the index moved and your loan’s cap structure.

Are 15-year fixed rates lower than 30-year fixed rates?

Yes — 15-year fixed mortgages typically come with a lower interest rate than 30-year fixed mortgages (often 0.50% to 0.75% lower). However, your monthly payment is higher because you’re paying off the loan in half the time. The total interest paid over the life of a 15-year loan is significantly less.

What is the break-even point when comparing ARM vs fixed?

The break-even point is when the total interest saved during the ARM’s initial fixed period equals the extra cost if rates rise afterward. If you’ll sell before the ARM adjusts, the ARM almost always wins on cost.

Final Thoughts

Choosing between a fixed and adjustable rate mortgage comes down to one core question: how long do you plan to stay in the home, and how much payment uncertainty can you handle?

If you value stability and are in it for the long haul, a fixed-rate mortgage gives you predictability and protection from rising rates. If you’re confident you’ll move or refinance within 5–7 years, an ARM can save you meaningful money with its lower introductory rate.

Either way, understanding how basis points affect your rate — and how even small differences compound over 30 years — puts you in a much stronger position at the negotiating table.

Related Calculators:

- Mortgage Calculator — estimate your monthly payment

- BPS to Percentage Calculator — convert basis points to a rate

- Loan Amortization Calculator — see your full payment schedule

- APR Calculator — find the true annual cost of your loan

Disclaimer: This article is for informational purposes only and does not constitute financial or mortgage advice. Please consult a qualified mortgage professional before making any lending decisions.