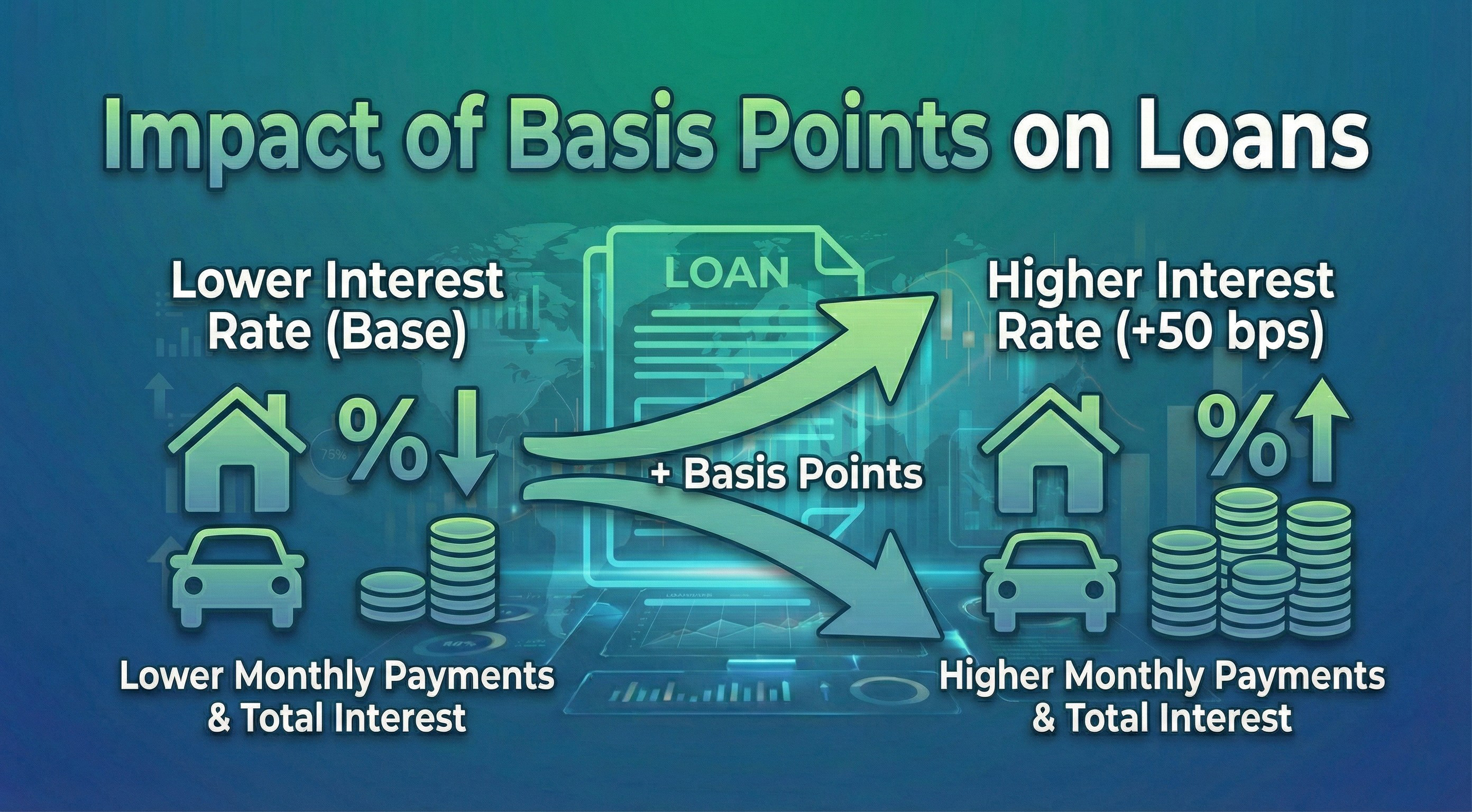

The Bottom Line: A seemingly small 25 basis point (0.25%) rate difference can cost you tens of thousands of dollars over the life of a mortgage. Always shop rates carefully!

Real Dollar Impact

Let’s look at how different rate changes affect a $300,000, 30-year mortgage:

| Interest Rate | Monthly Payment | Total Interest | vs 6.00% (extra cost) |

|---|---|---|---|

| 6.00% | $1,799 | $347,515 | Baseline |

| 6.25% (+25 bps) | $1,847 | $364,820 | +$17,305 |

| 6.50% (+50 bps) | $1,896 | $382,633 | +$35,118 |

| 6.75% (+75 bps) | $1,946 | $400,934 | +$53,419 |

| 7.00% (+100 bps) | $1,996 | $419,705 | +$72,190 |

Key Insight: Just 100 basis points (1%) higher rate costs an extra $72,190 in interest and adds nearly $200/month to your payment on a $300,000 loan.

Impact on Different Loan Types

- Mortgages: Long terms amplify the impact. 25 bps on a 30-year mortgage affects payment for decades.

- Auto Loans: Shorter terms reduce total impact, but 50 bps still means hundreds in extra interest.

- Credit Cards: High rates mean basis point changes are proportionally smaller but still significant on large balances.

- Student Loans: Extended repayment terms can make rate differences add up substantially.

Strategies to Get Lower Rates

- Improve credit score: 50 points can save 25-50 bps

- Shop multiple lenders: Rates can vary by 50+ bps between lenders

- Larger down payment: Lower loan-to-value often means lower rates

- Pay for points: Each point (1% of loan) typically lowers rate by 25 bps

- Shorter term: 15-year mortgages usually have lower rates than 30-year

When Basis Points Matter Most

Focus on rate shopping when:

- Large Loans: $250,000+

- Long Terms: 15+ years

- Variable Rates: Can change over time