Every bank, lender, and financial product throws three rate terms at you — and most people use them interchangeably by mistake. APR, APY, and interest rate are not the same thing. Using the wrong one to compare financial products can cost you real money: picking a savings account with a higher “interest rate” over one with a higher APY, or comparing two mortgage offers using APR when you should be looking at the base rate for your monthly payment.

This guide explains exactly what each term means, how they’re calculated, when each one applies, and — critically — which rate to look at for any given financial decision.

The Short Answer

| Term | Stands For | Includes Fees? | Includes Compounding? | Used For |

|---|---|---|---|---|

| Interest Rate | — | No | No | Base rate on loans & savings |

| APR | Annual Percentage Rate | Yes | No | Borrowing cost comparison |

| APY | Annual Percentage Yield | No | Yes | Savings & investment returns |

The relationship between them:

Interest Rate is the foundation. APR adds fees on top. APY adds compounding on top.

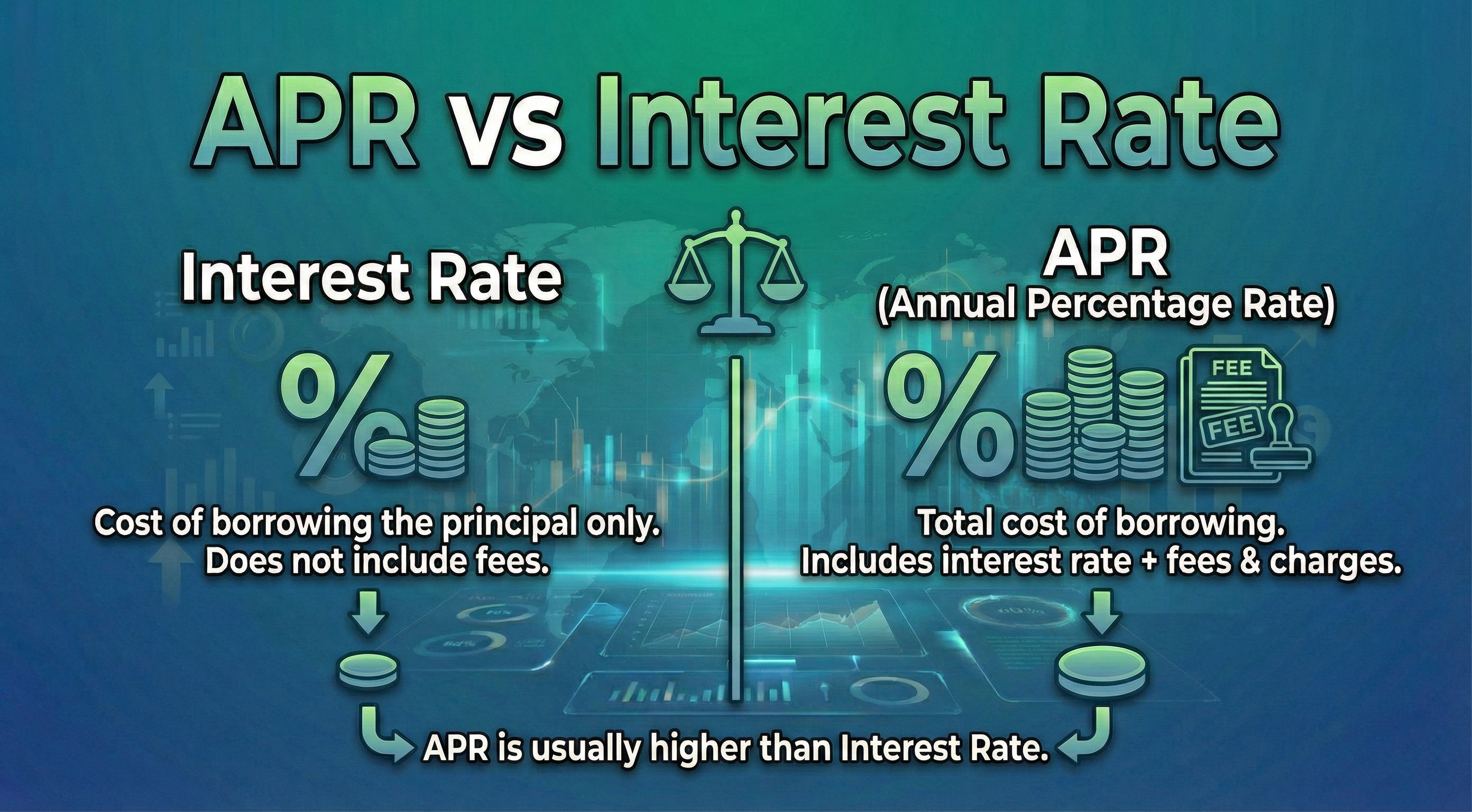

What Is an Interest Rate?

The interest rate (also called the nominal rate or stated rate) is the base percentage a lender charges you to borrow money — or a bank pays you to hold your money. It’s the raw rate before any fees are added or compounding is applied.

Key characteristics:

- Expressed as an annual percentage

- Does not include origination fees, closing costs, or other charges

- Does not account for how often interest compounds

- Appears in loan contracts and savings account disclosures

Example: You get a mortgage with a 6.00% interest rate. Every year, 6.00% of your outstanding principal accrues as interest — broken into monthly payments of 0.50% (6.00% ÷ 12).

The interest rate is the starting point for calculating both APR and APY, but it tells you less than either one does on its own.

What Is APR (Annual Percentage Rate)?

APR is the annual cost of borrowing money expressed as a percentage — and crucially, it includes fees that the interest rate alone doesn’t show. In the US, lenders are legally required to disclose APR under the Truth in Lending Act (TILA).

What APR includes:

- The base interest rate

- Origination fees

- Closing costs (on mortgages)

- Mortgage broker fees

- Discount points paid

- Certain other mandatory fees

What APR does NOT include:

- Appraisal fees (usually)

- Title insurance (sometimes)

- Prepayment penalties (sometimes)

- Optional add-ons

The APR formula:

APR = ((Fees + Total Interest) ÷ Principal ÷ Loan Term in Days) × 365 × 100

In practice, you never need to calculate this manually — lenders are required to provide it on every loan offer. But understanding what’s inside it helps you compare offers properly.

Example — same loan, two lenders:

| Lender A | Lender B | |

|---|---|---|

| Interest Rate | 6.25% | 6.00% |

| Origination Fee | $0 | $4,500 |

| APR | 6.25% | 6.48% |

Lender B has the lower stated rate but costs more overall once fees are counted. APR reveals this. If you only compared interest rates, you’d pick the wrong lender.

Important limitation: APR assumes you hold the loan for its full term. If you sell or refinance in 5 years, the fees are spread over a shorter period, making high-fee loans more expensive in practice than the APR suggests.

What Is APY (Annual Percentage Yield)?

APY is the effective annual return on a deposit or investment that accounts for compounding — earning interest on your interest. APY is always equal to or greater than the interest rate.

The APY formula:

APY = (1 + r/n)ⁿ − 1

Where:

- r = annual interest rate (as a decimal)

- n = number of compounding periods per year

Compounding frequency table:

| Compounding | n | 6.00% Rate → APY |

|---|---|---|

| Annually | 1 | 6.000% |

| Semi-annually | 2 | 6.090% |

| Quarterly | 4 | 6.136% |

| Monthly | 12 | 6.168% |

| Daily | 365 | 6.183% |

| Continuously | ∞ | 6.184% |

More frequent compounding = higher APY from the same stated rate. This is why banks often advertise APY rather than interest rate — it’s always the larger number.

Worked example:

You deposit $10,000 in a high-yield savings account with a 6.00% nominal rate, compounded monthly.

- Monthly rate: 6.00% ÷ 12 = 0.50%

- After 12 months: $10,000 × (1.005)¹² = $10,616.78

- APY: ($10,616.78 − $10,000) ÷ $10,000 = 6.168%

Without compounding (APR equivalent), you’d earn exactly $600. With monthly compounding, you earn $616.78 — an extra $16.78 just from interest-on-interest. On larger balances over longer periods, this difference becomes substantial.

APR vs APY: The Key Differences

These two are the most commonly confused pair. Here’s what separates them:

| APR | APY | |

|---|---|---|

| Used for | Loans, mortgages, credit cards | Savings accounts, CDs, investments |

| Includes fees | Yes | No |

| Includes compounding | No | Yes |

| Higher or lower? | Higher than interest rate (adds fees) | Higher than interest rate (adds compounding) |

| Regulated disclosure | Required for loans (TILA) | Required for deposits (TISA) |

| Goal | Show true borrowing cost | Show true earnings potential |

The critical rule: APR and APY are not directly comparable to each other. One is about the cost of borrowing, the other is about the return on saving. Never compare a loan’s APR to a savings account’s APY to evaluate a financial decision.

Interest Rate vs APY: Which Is Higher?

APY is always equal to or greater than the stated interest rate — never lower. The gap between them depends entirely on compounding frequency.

For savings accounts: Banks almost always advertise APY because it’s the larger, more attractive number. When comparing savings accounts, always compare APY to APY — never compare one bank’s APY to another’s “interest rate.”

Example:

- Bank A: 5.00% interest rate, compounded daily → APY: 5.127%

- Bank B: 4.90% interest rate, compounded monthly → APY: 5.012%

Bank A has the higher APY despite a seemingly small rate difference. APY is the only fair comparison.

Interest Rate vs APR: Which Matters for Your Mortgage?

Both matter — but for different decisions.

Use the interest rate to calculate your actual monthly payment. Mortgage payment calculators use the base interest rate, not APR.

Use APR to compare the total cost across different lenders. A lender with a lower rate but high fees may cost more over the life of the loan than one with a slightly higher rate and no fees.

Quick rule:

If you’re staying in the home long-term → APR matters more (amortizes fees over longer period) If you’re selling or refinancing within 5 years → Base rate matters more (fees hit harder relative to time held)

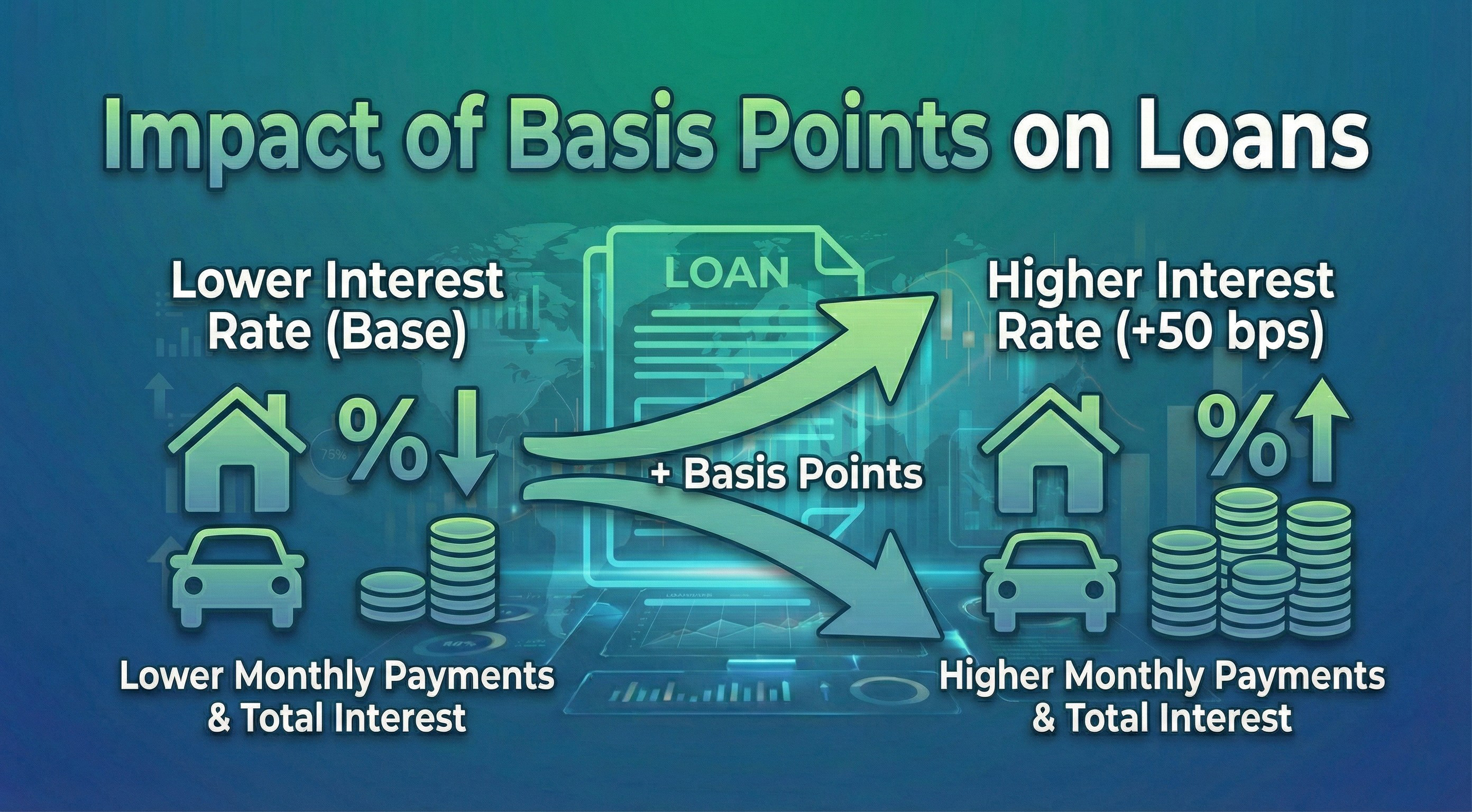

In basis points: A difference of 25 basis points in your mortgage rate equals approximately $750/year on a $300,000 loan. A $3,000 origination fee on the same loan becomes negligible after 4+ years but is significant if you move sooner.

Which Rate Should You Use?

Quick decision guide:

| Situation | Use This Rate | Why |

|---|---|---|

| Comparing mortgage lenders | APR | Includes fees for fair comparison |

| Calculating monthly payment | Interest Rate | Base rate drives amortization |

| Comparing savings accounts | APY | Includes compounding for fair comparison |

| Comparing CDs | APY | Same reason |

| Evaluating investment returns | APY | Shows real compounded growth |

| Credit card cost comparison | APR | No compounding benefit to borrowers |

| Short-term loan (under 2 years) | APR carefully | Fees dominate short-term cost |

Real-World Scenarios

Scenario 1: Picking a High-Yield Savings Account

You’re comparing three online banks:

| Bank | Advertised Rate | Compounding | APY |

|---|---|---|---|

| Bank A | 4.75% | Monthly | 4.849% |

| Bank B | 4.80% | Quarterly | 4.893% |

| Bank C | 4.70% | Daily | 4.807% |

Bank B wins despite not having daily compounding — quarterly compounding on a slightly higher rate produces the best APY. Always compare APY directly, not the advertised rate.

Scenario 2: Choosing Between Two Mortgages

$400,000 loan, 30-year term:

| Option A | Option B | |

|---|---|---|

| Interest Rate | 6.75% | 6.50% |

| Origination Fee | $0 | $6,000 (1.5%) |

| APR | 6.75% | 6.73% |

| Monthly Payment | $2,594 | $2,528 |

| Monthly Savings | — | $66/mo |

| Break-even on fees | — | $6,000 ÷ $66 = 91 months |

Option B has the lower APR, but only makes sense if you stay for 91+ months (7.6 years). If you plan to sell or refinance sooner, Option A is cheaper despite the higher stated rate.

Scenario 3: Understanding a Credit Card

Your credit card has a 24.99% APR. Since credit card interest compounds daily:

- Daily rate: 24.99% ÷ 365 = 0.06847%

- Effective APY: (1 + 0.006847/100)³⁶⁵ − 1 = 28.4%

This is why carrying a credit card balance is so costly — the effective rate (APY) is nearly 3.5 percentage points higher than the advertised APR.

How Basis Points Connect All Three Rates

In professional finance, differences between APR, APY, and interest rates are expressed in basis points (bps) — because the gaps are often small but financially significant.

- A savings account with 12 bps higher APY = meaningfully better over time

- A mortgage with 25 bps lower APR = ~$750/year on a $300,000 loan

- A credit card with 50 bps lower APR = noticeable savings on revolving balances

Understanding basis points lets you evaluate whether a difference in APR or APY is actually worth switching products. A 10 bps APY improvement on a $50,000 savings account = $50/year — possibly not worth moving. A 50 bps APR improvement on a $400,000 mortgage = $2,000/year — almost always worth shopping for.

Use our free Basis Point Calculator to instantly see the dollar impact of any rate difference in basis points.

Frequently Asked Questions

Is APY the same as APR?

No. APR (Annual Percentage Rate) measures the cost of borrowing and includes fees but not compounding. APY (Annual Percentage Yield) measures the return on savings and includes compounding but not fees. They are not directly comparable because they serve different purposes.

Is a higher APY better?

For savings and investments, yes — a higher APY means more money earned per year. Always compare APY to APY when evaluating savings accounts, CDs, or money market accounts.

Is a lower APR better for loans?

Yes — a lower APR means a lower total cost of borrowing, since it includes fees. However, also check the base interest rate if you want to compare monthly payment amounts, and factor in how long you plan to keep the loan.

Why is my APY higher than my interest rate?

Because APY accounts for compounding — earning interest on your interest. The more frequently interest compounds (daily vs. monthly vs. annually), the higher the APY relative to the stated interest rate.

Can APR be lower than the interest rate?

No. APR is always equal to or higher than the interest rate because APR adds fees on top of the base rate. If you ever see an APR lower than the interest rate, it’s either a calculation error or a promotional/adjustable rate situation.

What is a good APY for a savings account?

This depends on the current interest rate environment. As a rule of thumb, compare any offered APY against the current federal funds rate and the average high-yield savings account rate in the market at that time. In 2024–2026 conditions with rates above 4%, any savings account APY below 4.00% would be considered below-average.

How do I convert APR to APY?

Use the formula: APY = (1 + APR/n)ⁿ − 1, where n is the number of compounding periods per year. For monthly compounding: APY = (1 + APR/12)¹² − 1. For a 6.00% APR compounded monthly: APY = (1.005)¹² − 1 = 6.168%.

Why do banks show APY but lenders show APR?

Regulations require it. The Truth in Lending Act (TILA) requires lenders to disclose APR on loans. The Truth in Savings Act (TISA) requires banks to disclose APY on deposit accounts. This is intentional — APY is the larger number for savings (banks want to attract depositors), and APR is the standardized cost comparison for borrowing.

Summary: APR vs APY vs Interest Rate

| Interest Rate | APR | APY | |

|---|---|---|---|

| Definition | Base rate charged or paid | Rate + all mandatory fees | Rate + compounding effect |

| Always higher than rate? | — | Yes (unless no fees) | Yes (unless no compounding) |

| Primary use | Payments, base comparison | Loan cost comparison | Savings account comparison |

| Regulated disclosure | No | Yes (TILA) | Yes (TISA) |

| Formula | — | (Fees + Interest) ÷ Principal | (1 + r/n)ⁿ − 1 |

| Expressed as | % per year | % per year | % per year |

The bottom line: use APR when borrowing, use APY when saving, and understand the interest rate behind both. When in doubt, always ask the lender or bank to clarify which rate they’re quoting and what it includes.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Always consult a qualified financial professional before making borrowing or investment decisions.