When your lender says “one point,” they could mean two very different things — and confusing them is one of the most expensive mistakes a homebuyer can make.

“Mortgage points” and “basis points” both use the word point, but they operate on completely different scales, serve different purposes, and have different cost implications. A single mortgage point on a $400,000 loan costs you $4,000 out of pocket. A single basis point changes your rate by just 0.01%. Mixing them up can distort your understanding of a loan offer by a factor of 100.

This guide breaks down both terms clearly, shows you exactly what each costs, and helps you decide whether paying mortgage points makes sense for your situation.

What Are Mortgage Points?

A mortgage point (also called a discount point) is a fee paid upfront at closing equal to 1% of your loan amount. You pay points to “buy down” your interest rate — essentially prepaying interest to get a lower monthly payment for the life of the loan.

1 mortgage point = 1% of loan amount = typically −25 basis points off your rate

The key word is typically. Lenders vary: some offer more rate reduction per point, others less. Always ask your lender exactly how many basis points each point buys on your specific loan.

How Much Do Mortgage Points Cost?

The cost scales directly with your loan size. Here’s what 1 and 2 points cost across common loan amounts:

| Loan Amount | 1 Point (1%) | 2 Points (2%) | 3 Points (3%) |

|---|---|---|---|

| $150,000 | $1,500 | $3,000 | $4,500 |

| $250,000 | $2,500 | $5,000 | $7,500 |

| $400,000 | $4,000 | $8,000 | $12,000 |

| $600,000 | $6,000 | $12,000 | $18,000 |

Points are paid at closing alongside your down payment and other closing costs. They are typically tax-deductible as prepaid mortgage interest — consult a tax professional for your specific situation.

What Are Basis Points?

A basis point (bps) is a unit of measurement equal to 0.01% — one one-hundredth of a percentage point.

1 basis point = 0.01% = 0.0001

Basis points are used throughout finance to describe small changes in interest rates precisely and unambiguously. When the Federal Reserve raises rates by “25 basis points,” that means rates increased by 0.25%. When a lender quotes your rate at “650 basis points,” they mean 6.50%.

Unlike mortgage points, basis points have no direct dollar cost attached to them — they simply describe a rate or a rate change.

Mortgage Points vs Basis Points: The Key Differences

These two terms share a name but almost nothing else:

| Mortgage Point | Basis Point (bps) | |

|---|---|---|

| What it is | An upfront fee | A unit of measurement |

| Size | 1% of loan amount | 0.01% |

| Has a dollar cost? | Yes — paid at closing | No |

| Purpose | Reduces your interest rate | Measures rate changes |

| Example | 1 pt on $300k = $3,000 | Rate rose 25 bps = +0.25% |

| Who uses it | Mortgage lenders | Lenders, Fed, markets |

The connection between them: when you pay 1 mortgage point, your lender typically reduces your rate by approximately 25 basis points (0.25%). That relationship is what makes the break-even analysis work.

How Basis Points Translate Into Monthly Savings

Understanding basis points helps you evaluate how much rate reduction you’re actually getting per point paid.

For a $250,000, 30-year mortgage:

| Rate (from → to) | Change (bps) | Monthly Payment Change | Annual Savings |

|---|---|---|---|

| 7.00% → 6.75% | −25 bps | −$44/mo | ~$528/yr |

| 7.00% → 6.50% | −50 bps | −$87/mo | ~$1,044/yr |

| 6.50% → 6.25% | −25 bps | −$41/mo | ~$492/yr |

| 6.25% → 6.00% | −25 bps | −$40/mo | ~$480/yr |

Every 25 basis points of rate reduction saves roughly $40–$45 per month on a $250,000 loan. The larger your loan, the more each basis point is worth to you in monthly savings.

The Break-Even Analysis: When Do Points Pay Off?

Paying mortgage points is only worth it if you stay in the home long enough to recoup the upfront cost through your monthly savings. This is called the break-even point.

Formula:

Break-Even (months) = Upfront Cost ÷ Monthly Savings

Example: $250,000 loan, 1 point paid ($2,500), rate drops 25 bps (6.50% → 6.25%), monthly savings = $41

Break-even = $2,500 ÷ $41 = 61 months (~5 years)

If you sell or refinance before month 61, you’ve paid $2,500 upfront but haven’t saved enough to cover it. If you stay longer, every month after break-even is pure savings — netting $2,420 over a 10-year horizon in this example.

Should You Pay Mortgage Points?

The answer depends almost entirely on how long you plan to stay in the home.

Three other factors to weigh:

1. Cash position at closing If paying points stretches your cash reserves, skip them. You’ll need reserves for emergencies, maintenance, and potential job changes. A lower rate won’t help if you’re house-poor.

2. Refinance likelihood If rates drop significantly in the next few years, you’ll likely refinance — resetting the break-even clock to zero. In uncertain rate environments, points are a riskier bet.

3. Your loan size The larger the loan, the more valuable each basis point of rate reduction becomes. On a $600,000 loan, 25 bps saves ~$96/month — meaning break-even on a $6,000 point happens in just 63 months. On a $150,000 loan, the same point costs $1,500 but saves only ~$24/month — break-even is also about 63 months. Scale matters, but the ratio stays similar.

A Complete Example: $300,000 Loan, 30 Years

Scenario: You’re buying a $375,000 home with 20% down ($300,000 loan). Your lender offers two options:

| Option | Rate | Points Paid | Upfront Cost | Monthly Payment | Monthly Savings |

|---|---|---|---|---|---|

| A (No points) | 6.75% | 0 | $0 | $1,945 | — |

| B (1 point) | 6.50% | 1 | $3,000 | $1,896 | $49/mo |

| C (2 points) | 6.25% | 2 | $6,000 | $1,847 | $98/mo |

Break-even analysis:

- Option B: $3,000 ÷ $49 = 61 months (5.1 years)

- Option C: $6,000 ÷ $98 = 61 months (5.1 years)

In this case, both options have similar break-even timelines. If you plan to stay 7+ years, Option C maximizes long-term savings. If there’s any chance you’ll move in under 5 years, stick with Option A and keep your $3,000–$6,000.

Frequently Asked Questions

Are mortgage points the same as origination points?

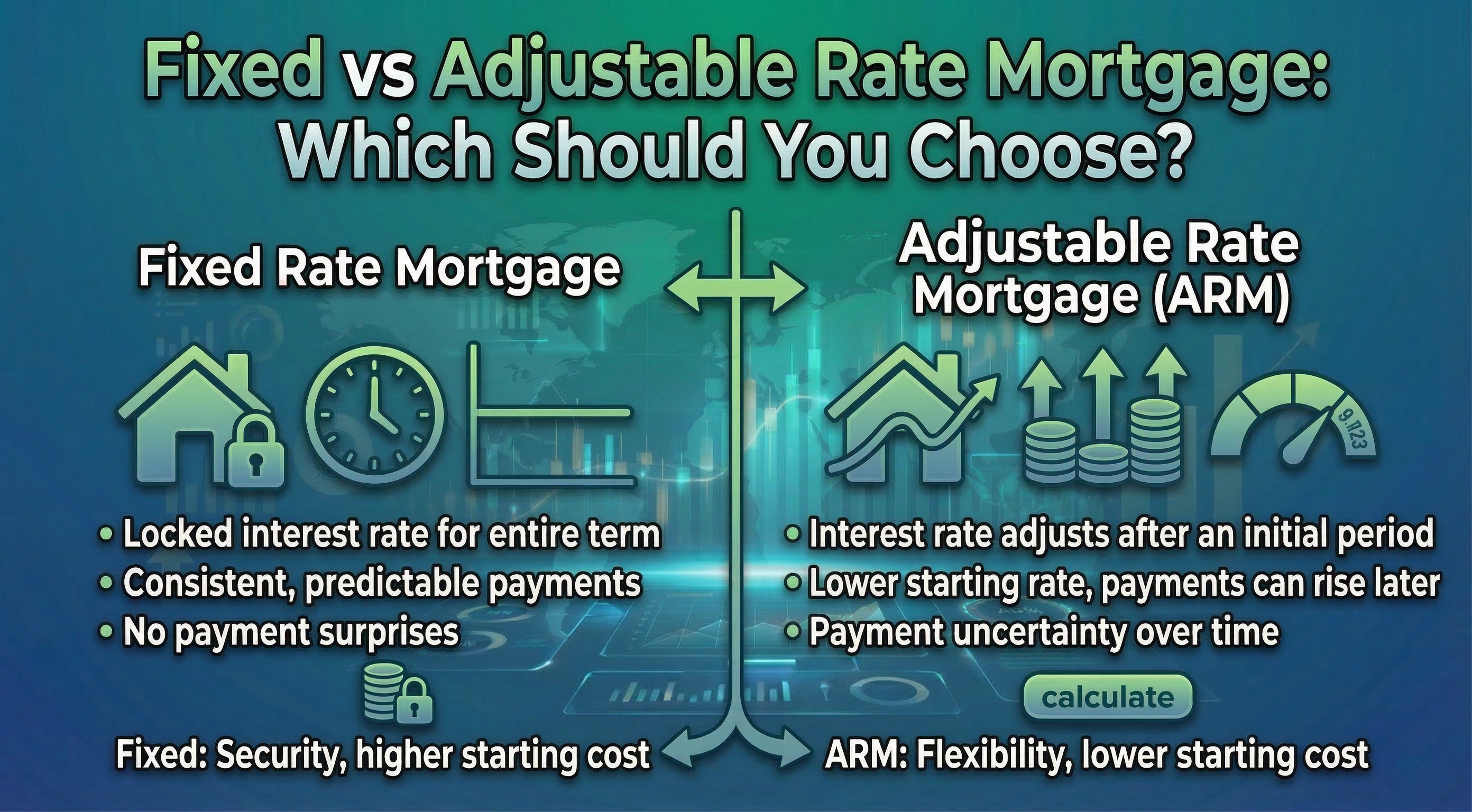

No. Discount points are optional fees paid to reduce your interest rate. Origination points (or origination fees) are what lenders charge to process your loan — they don’t reduce your rate. Always ask your lender which type they’re quoting.

How many basis points does 1 mortgage point typically buy?

Most lenders offer approximately 25 basis points (0.25%) of rate reduction per point paid, but this varies. Some lenders offer only 12–20 bps per point. Always confirm the exact rate reduction before paying.

Can you pay partial points?

Yes. You can pay 0.5 points, 1.5 points, or any fraction. Half a point on a $300,000 loan costs $1,500 and typically buys down your rate by about 12–13 basis points.

Are mortgage points tax-deductible?

In many cases, yes — discount points paid on a home purchase are deductible as prepaid mortgage interest in the U.S. However, tax rules change frequently. Consult a qualified tax advisor for your specific situation.

What’s a “no-cost” mortgage?

A no-cost mortgage means the lender covers your closing costs, but in exchange your interest rate is higher — typically by 25–75 basis points. You’re essentially paying the closing costs through a slightly higher rate over time rather than upfront.

Is it better to pay points or make a larger down payment?

This depends on your situation. A larger down payment reduces your loan principal (and potentially eliminates PMI), while points reduce your rate. Run the numbers for both scenarios — in most cases, eliminating PMI first provides more immediate savings.

What does it mean when rates are quoted “in basis points”?

Lenders and financial professionals use basis points to describe small rate differences precisely. If one lender quotes 6.50% and another quotes 6.625%, the difference is 12.5 basis points. Thinking in basis points prevents the ambiguity of saying a rate is “a little higher.”

Quick Reference: Key Formulas

| What You Want | Formula |

|---|---|

| Cost of 1 mortgage point | Loan Amount × 0.01 |

| Rate reduction from N points | N × ~0.25% (lender-specific) |

| Monthly savings from rate drop | Use a mortgage calculator |

| Break-even in months | Upfront Cost ÷ Monthly Savings |

| Convert rate to basis points | Rate (%) × 100 |

| Convert basis points to rate | BPS ÷ 100 |

Final Thoughts

Mortgage points and basis points are both called “points,” but they operate at completely different scales and serve entirely different purposes. Mortgage points are a financial decision — an upfront cost that may or may not pay off depending on how long you stay. Basis points are a measurement tool — a precise way to describe tiny rate movements.

The most important takeaway: before paying any mortgage points, calculate your exact break-even date and compare it honestly to how long you expect to stay in the home. If the numbers don’t work, keep the cash.

Use our free Basis Point Calculator to instantly convert between basis points, percentages, and decimals — and to model how rate changes affect your monthly payment.

Disclaimer: This article is for educational purposes only and does not constitute financial or tax advice. Always consult a qualified mortgage professional and tax advisor before making borrowing decisions.